Grift 2.1: MicroStrategy’s Clone Wars Begin

Are We Ready for Another Wall Street Round of 1 + 0 = 2? FOMO Says Yes!

In order to make an enormous profit in a public Bitcoin offering, Michael Saylor is being cloned.

In 2020, Saylor and his once-forgotten tech firm called MicroStrategy (MSTR) did something very very bold. He turned his software company into a Bitcoin vault. He mortgaged the business, borrowed billions, bought Bitcoin hand over fist and told the world it was all part of a brilliant new “Strategy.”

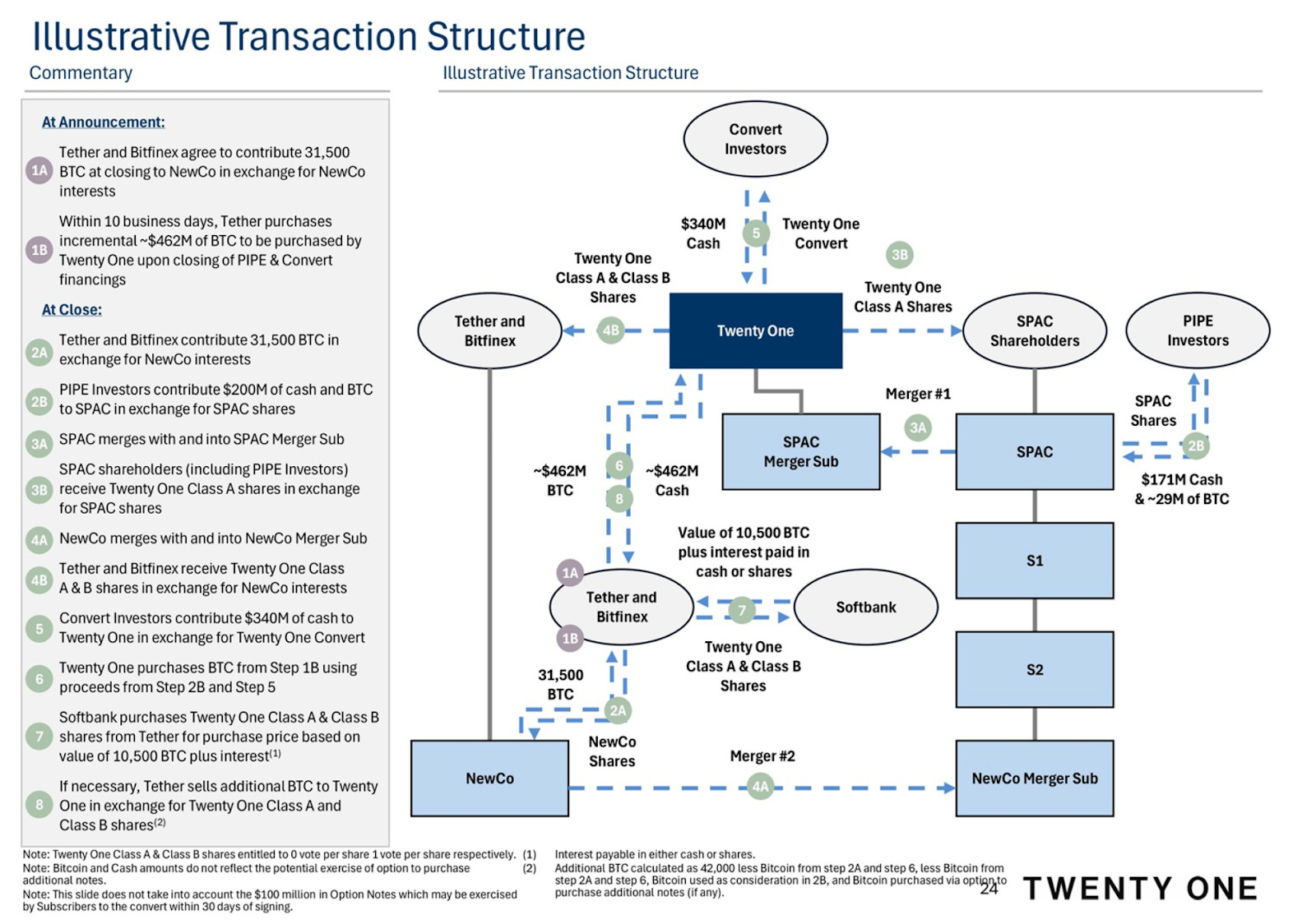

A proposed $3 billion deal between a crypto investment vehicle called TwentyOne and a SPAC called Cantor Equity Partners (CEP) is the first real attempt to copy Saylor’s playbook at scale. Buying Bitcoin.

At first glance, it all looks eerily familiar. Borrow money. Buy Bitcoin. Tell a story. Watch your stock soar.

Meet the New Bitcoin Apostles

The cast of characters reads like a crossover special of Billions and American Greed:

Brandon Lutnick: Son of the former CEO of Cantor Fitzgerald, and now apparently running the family SPAC business as dad moves into public service under President Trump.

Tether/Bitfinex: the mysterious operators of USDT, a “stablecoin” that has been dogged for years by questions over what actually backs its promised 1:1 peg to the dollar. Spoiler: not always dollars.

SoftBank: Represented here by Masayoshi Son, the man who gave the world Vision Fund, WeWork, and perhaps the most expensive masterclass in FOMO in financial history.

Together, they’ve built a new kind of SPAC. One that doesn’t even pretend to be interested in finding a hot new startup or a future-of-tech unicorn. This one just wants to buy Bitcoin — and then watch people pay a premium to own the Bitcoin they already could’ve bought themselves.

Is the SPAC Back?

The FT’s Lex columnist John Foley seems to think so.

And it would make sense in what one commentator has called “the Golden Age of Grift”:

The Stock Market during the Golden Age of Grift is a device for transferring money from the Outsiders to the Insiders

SPACs (Special Purpose Acquisition Companies), in theory, are blank-check companies that raise money from public investors and then rush to find a private company to take public. In practice, they’ve become tools for insiders to extract wealth from outsiders.

The senior Lutnick (see above) is famous for being the second biggest opportunist – though well short of Chamath – in SPACs the last time around. For a nominal investment of $150,000 he acquired stakes worth $600,000,000 at IPO:

During the 2020–2021 boom, SPAC sponsors made hundreds of millions on tiny capital contributions. They got in early, picked the target, and walked away rich — while the average post-merger investor (the poor soul who actually believed the pitch) lost big. Has any asset class performed this badly? -88% since 2020.

The last SPAC cycle ended in a dumpster fire of overhyped electric vehicle companies, fitness apps, and one flying taxi startup that couldn’t actually fly.

But TwentyOne is different. It’s not even pretending to build a business. It’s not selling space, software, jets, or spin bikes. It’s selling Bitcoin with a wrapper — and that wrapper is the story.

MicroStrategy.

If you want to understand the logic behind all this, you have to go back to MicroStrategy (now simply “Strategy”).

MSTR’s operating business has been bleeding money for years. Revenue is stagnant. EBITDA is negative. Net income has mostly been a rounding error. But none of that has mattered since Saylor turned the company into a Bitcoin-buying machine.

Today, MSTR trades at more than 2x the value of the Bitcoin it owns. Investors pay a premium for the privilege of owning crypto via a public company. Why?

It’s eligible for tax-advantaged accounts. (But so are ETFs).

It’s index-eligible: NASDAQ 100, soon S&P 500?. (But stocks can exit indices as fast they enter).

It leverages with fixed low-interest borrowings. (A double edged sword).

It’s a bet on Saylor’s timing — and so far, he’s nailed it. (For how much longer?).

Raising capital at a premium is accretive. (A self-fulfilling prophecy).

But what do I know? Investors believe. Since 2020, MicroStrategy has outperformed almost every major asset — including the AI darling NVIDIA.

It’s shocking it took this long to attract competitors to the MSTR business model. I mean, if you can buy Bitcoin and immediately double your investment, why wouldn't you?

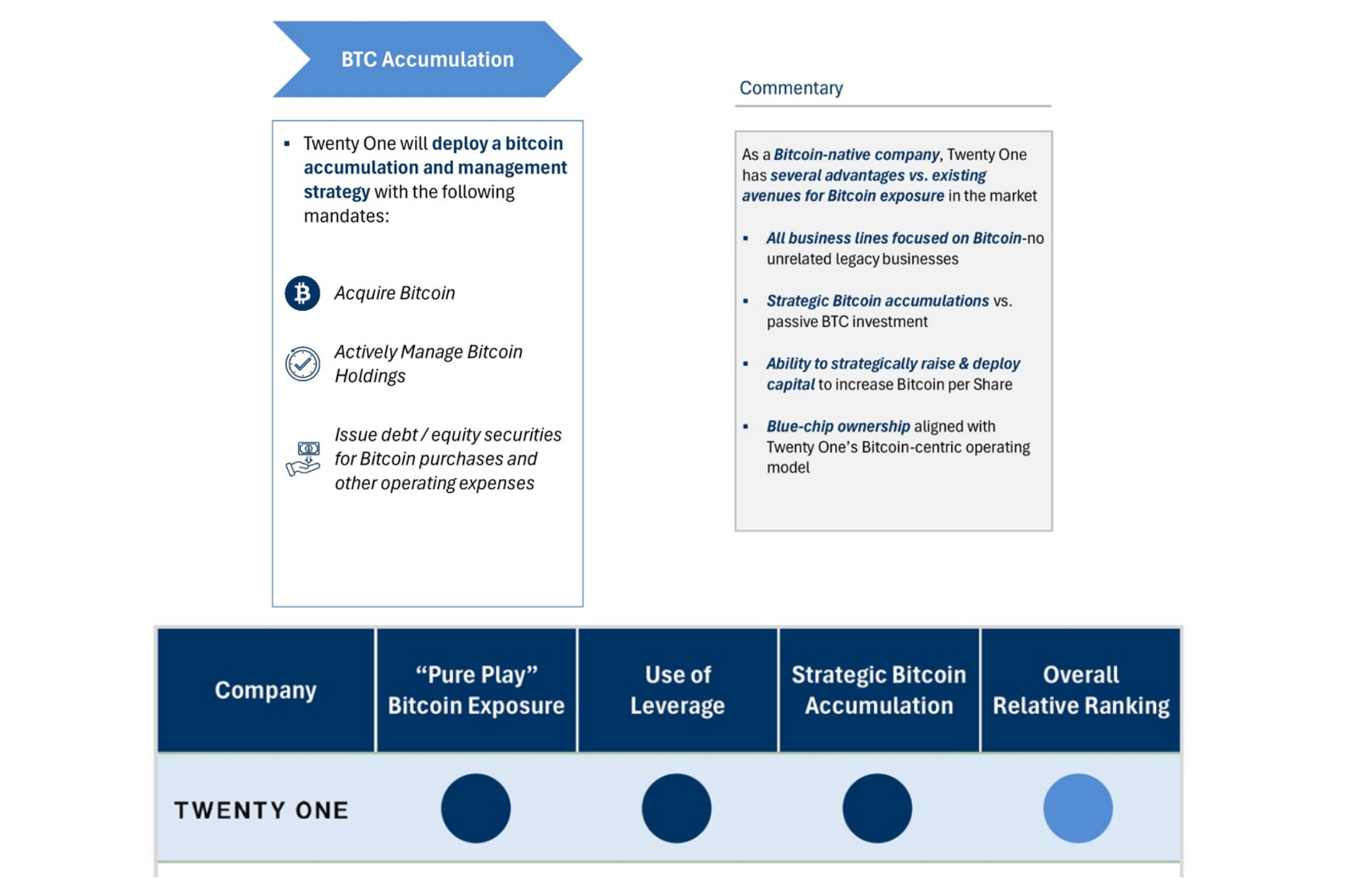

So What’s TwentyOne Actually Doing?

Nothing fancy. Just copytrading MSTR but without the burden of having an underperforming SaaS business.

They’ll raise billions. Buy Bitcoin. Borrow more money. Buy more Bitcoin. Maybe lend it out. That’s it.

It is, unapologetically, a one-trick pony. Or as they put it: “A singular vehicle for Bitcoin exposure.”

To insiders, convert buyers and PIPE (private investment in public equity) investors, there is little downside: get $10 worth of Bitcoin for $10 — or less, depending on structure.

But the expectation is clear: retail investors will pay far more. Potentially even more than Saylor fans.

Does This Make Any Sense?

No.

A vehicle that simply holds Bitcoin should trade near the value of its Bitcoin.

Hype is a hell of a drug. But structurally, there’s nothing here to justify the premium — no earnings, no business, no moat.

What TwentyOne is really selling is the idea that lightning strikes twice.

But only twice.

The issue is that NAV premium goes away once competitors to MSTR enter. And this new SPAC shows they can. And will.

Will it Work?

If TwentyOne/Cantor Equity Partners can reach the same audience and concoct the same alchemy as MSTR, they could double their ten-figure investment. Overnight.

That would be a $3.6 billion payday for doing very little.

However, the only justification for a premium is the belief that the new guys — Jack Mallers, the nominal face of TwentyOne, or the Lutnick-Son-Tether dream team — can somehow both time the market and use any leverage optimally and without putting the company at risk.

Could they?

Maybe. For a while.

In any event the hype is working.

Cantor Equity Partners is trading around $47.70. That’s nearly 5x NAV. For context: even at the peak of the MicroStrategy mania, it briefly hit 5–6x. Briefly. At the start of its hype cycle.

So that’s where we are.

1 + 0 = 5

By the numbers:

$3.6 billion to buy Bitcoin.

$10 (actually slightly less) a share NAV.

$47.70 stock price.

Old math, at MSTR: 1 + 0 = 2.

New math, in the golden age of grift and hype: 1 + 0 = 5.

The original efficient market theorists must be turning in their grave.

Michael Saylor built a cult. These new guys are profiting.

Maybe it really is SPAC 2.0 season.

But 5x NAVs rarely last for long.