What Didn’t Happen in the Bond Market

Caution: Bond geek at work.

When the world’s biggest market speaks, it’s worth listening.

The US Treasury Bond market was roiling last week. April 9th’s $2.44 trillion was a trading volume record, breaking all previous records on consecutive days. Treasury bond futures volumes also surged to new highs.

As has been pointed out just about everywhere, the end result was that US interest rates reversed course and abruptly rose last week — even though they typically fall during market corrections. Rather than reflecting a normal flight-to-quality, the US behaved like an emerging market, with bonds, stocks, and the dollar all falling in unison on the week.

The business media quickly identified a scapegoat for the rise in bond yields: the 'basis trade.'

A likely contributor is the unwinding of the 'basis trade'—a high-risk, highly leveraged hedge fund strategy that exploits price differences between Treasury bonds and their futures contracts.

— Barron's, April 8, 2025

But does the evidence support this theory? No.

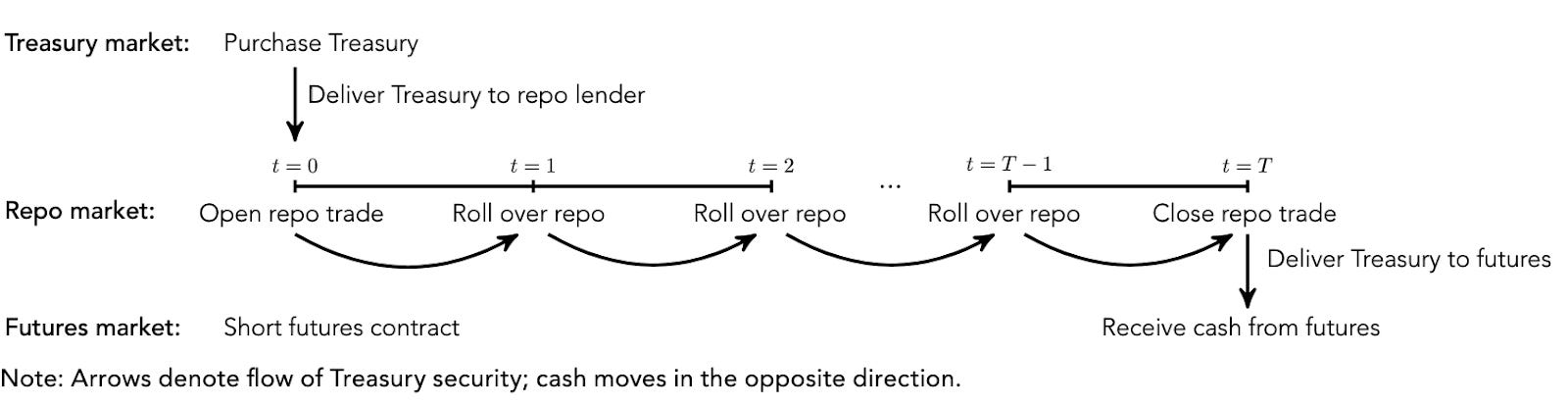

Basis Trading Explained

Basis trading involves taking offsetting positions in a Treasury bond and its related futures contract, aiming to profit from small pricing discrepancies that tend to close as the futures approach maturity.

The cash-and-carry trade is long bonds, funded in the repo market, and short futures. The repo market, which provides collateralized funding for bond purchases, is rolled daily.

Eventually, the Treasury futures price will converge with the spot price. The bonds can then be delivered into the futures contract, unwinding the trade.

It’s nearly risk free. Only the repo rate is unknown and therefore a source of risk.

As such, in an ideal world without financing frictions, this combo would behave like a Treasury bill, but with a yield advantage to compensate for financing risks, including repo rate volatility.

Bonds Fall. Hedge Funds Blamed

The trade offers modest profit margins but is often executed with 25–50x leverage, juiced by cheap repo financing. Positions leveraged by such enormous multiples need to be unwound if the trade moves even slightly against the arbs.

This happened at least once before, in 2020. At that time, the exposure hedge funds faced was only one third of the over $1 trillion they had on the books in March. So it seems plausible that the rise in yields could have been attributed to a recurrence of the 2020 basis trade unwind.

But where is the evidence? Most of those pointing fingers have no insider information pointing to such an unwind, while other commentators cite indirect signals that prove nothing on their own.

Let’s look at the direct evidence.

The Dog Did Not Bark

Despite widespread finger-pointing at hedge funds, clear evidence for their culpability is surprisingly thin. To test the "basis unwind" theory, we need to check for certain tell-tale signs. Did we see those signs? No. The dogs did not bark.

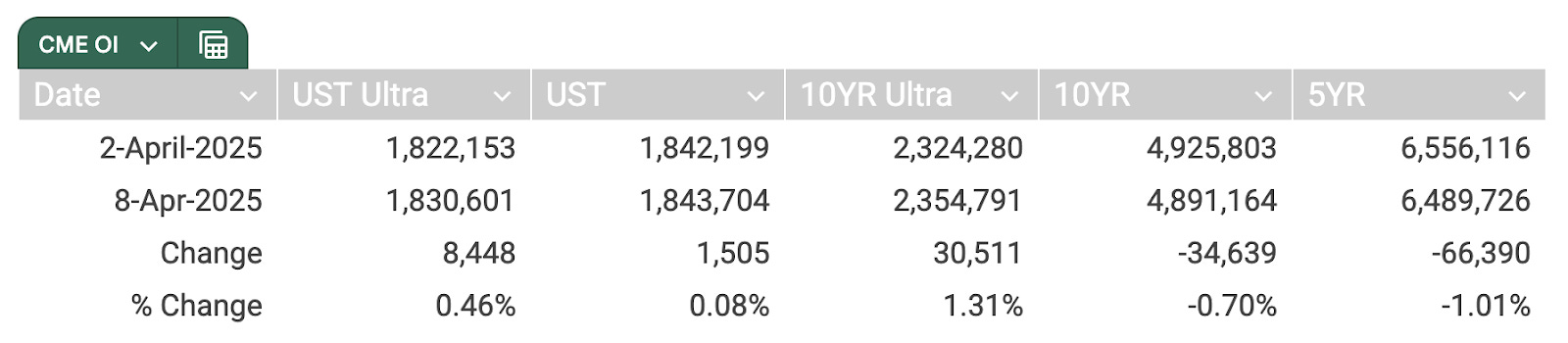

1. Futures Open Interest

As hedgies closed out their trades — selling cash bonds and covering their short futures — open interest (OI = number of futures contracts outstanding) in futures for each contract should have dropped. At the very least, short OI held by leveraged funds would have fallen off a cliff, as it did – by 15% – in the last major basis dislocation, in March 2020. But neither situation occurred last week.

Open interest in long bond and 10-year note futures remained largely unchanged:

Less than a one percent change overall.

In March 2020, short interest held by leveraged funds collapsed as the basis trade was unwound. As of the April 8th CFTC Commitment of Traders, hedge fund short interest was largely unchanged. Leveraged funds actually went a little more short in the 10yr:

There was no fire-sale closing of hedge fund positions visible in the data.

2. Relative Bond Value

To unwind the basis trade, hedge funds have to sell the bond that is used in the arbitrage, called – for reasons we won’t get into today – the cheapest to deliver (CTD). The CTD tracks the futures contract most closely, as it is the bond that will be delivered upon the expiry of the futures contract that is short.

If the arb is working, the CTD is expensive to buy, trading at a yield premium to similar bonds around it on the yield curve. When the trade is being unwound, the CTD bonds should get cheaper as they are being liquidated.

That didn’t happen. The cheapest to deliver did not cheapen up to the rest of the curve. JPMorgan noted in a research piece that most CTD bonds underlying the CME futures contracts hardly budged in relative value last week. The US Treasury CTD actually tightened by four basis points. No indication of forced selling here.

3. Basis Return Dynamics

If there were stress in the system and/or there were massive basis trade unwinds, the gross return to being long bonds and short futures should have widened. In other words, futures would rally relative to cash bonds as traders closed shorts.

How did the implied repo rate behave last week? It rose on average but showed no signs of distress. The return to going long the cash-and-carry basis trade rose modestly, by six basis points, for the US Treasury bond basis, and actually fell for the five year. The exception was the Ultra (30 year) Treasury bond basis, which rose by 30 basis points. That’s meaningful at 50x leverage, but far from catastrophic.

4. Repo Market Stress

The actual repo rate was unchanged on the week. There was no liquidity stress on the basis trade. Bonds were as easy to borrow against on April 8th as they were on April 2, again according to JPMorgan.

As a result, the SOFR - Fed Funds spread averaged 0.05% last week — nearly identical to the prior week’s 0.055% — even as the long bond yield rose over 40 basis points.

No stress here.

So What Is Happening?

The truth? No one really knows why the bond market is this unhappy. After listing the basis trade as one of the potential causes of the fall in Treasury prices, one commentator finally admitted:

But we can say that while the markets moved, the basis trade didn’t.

Why does it matter that the hedge funds got blamed? Well, the alternative is not very complimentary to recent US policy. Maybe we’re in a 1970s-like crisis. Though generally bonds and stocks move in opposite directions in highly volatile markets, between 1972 and 1974, gold surged 129%, Treasuries dropped 11%, and stocks fell 50% over 21 months, according to AQR’s Antti Ilmanen.

Back then, it was the collapse of Bretton Woods (and the dollar devaluing), OPEC-driven inflation shocks, and a crisis of confidence in U.S. leadership (Nixon et al).

Sound familiar?

So it’s easier to cite “technical factors” such as the basis trade rather than face the possible hard truth that markets are very unhappy with the direction of the US economy and policy.

Blaming greedy faceless billionaire hedge fund managers distracts from what is really behind the curtain.